Collaborating and Competing in the Brave New Biotech World

Tony Jones, CEO, One Nucleus, Email: [email protected]

Is it new, another cycle or evolution of the biotech sector?

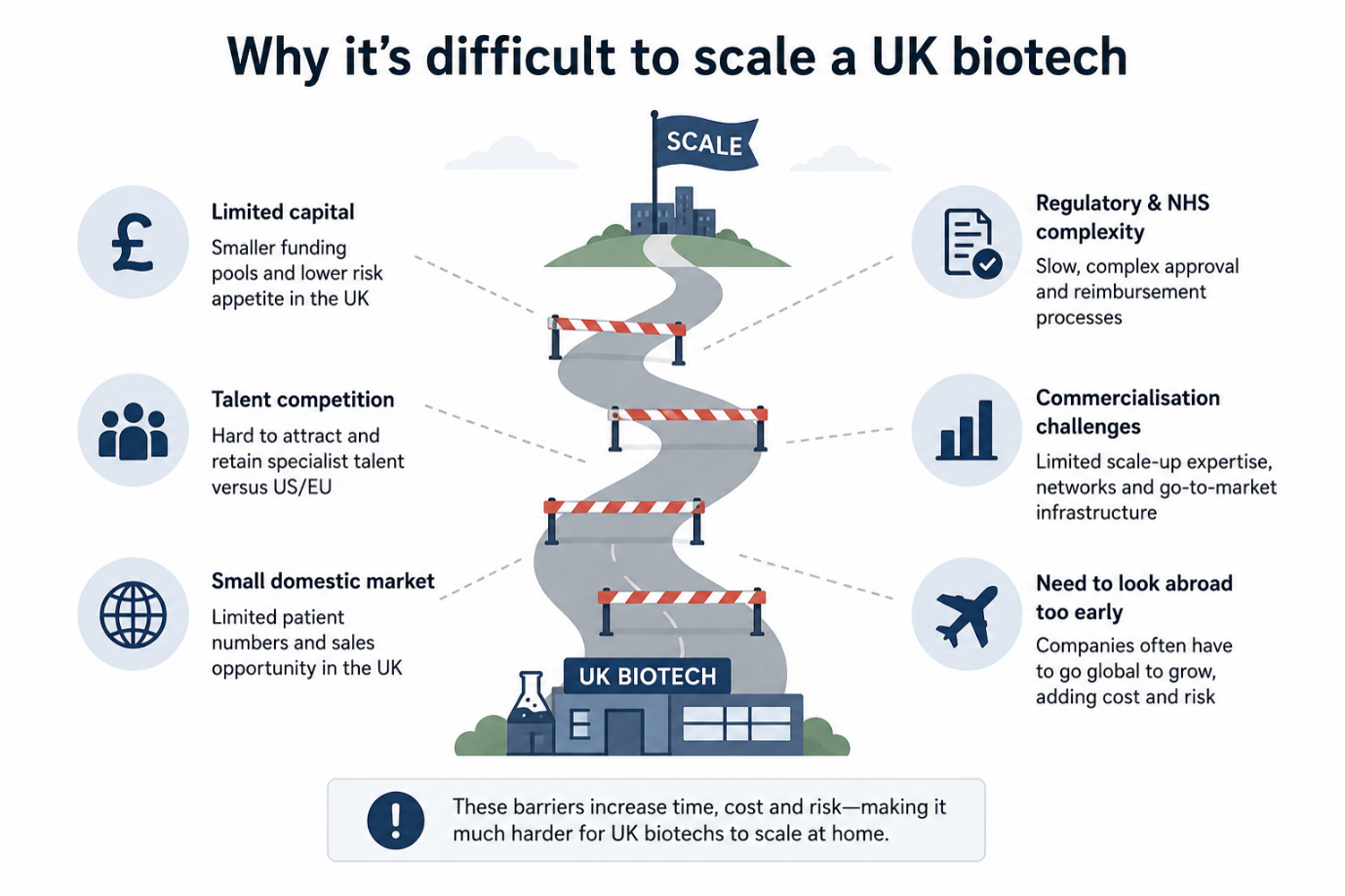

There have always been many pressures on the biotech industry innovation process. Limitations of existing technologies, sufficient understanding of biology, investment gaps, lack of available lab space to scale, lack of available talent to scale, changing regulations and more. Each of these hurdles has been addressed to a greater or lesser degree in numerous cycles throughout the decades of the biotechnology industry to date. Often when one aspect is less of a challenge, others are more significant, and innovators, biotech leaders and investors navigate that balance repeatedly.

Recent years have seen a prolonged period of scarcity of investment, particularly into early-stage drug discovery, where that dynamic is persisting compared to clinical-stage assets.

Current Landscape:

Phrases often voiced when C-suite leaders and their peers explore options include ‘capital efficiency’, ‘speed to data’, and ‘be more virtual’. These are absolutely real pressures, and it is likely no sector exits a time of financial hardship as it entered it. Evolving to adopt these desired attributes will build on some experiences of the past. Neither virtual biotech companies nor outsourcing to reduce cost or increase speed are new by any stretch of the imagination. Equally, the drive to scale-up UK biotechs, both politically to drive economic development and commercially to increase investor returns in the UK, remains strong yet still faces the same challenges. It should be noted that policy developments at MHRA, the UK government and others are seeking to address several of these barriers.

Phrases often voiced when C-suite leaders and their peers explore options include ‘capital efficiency’, ‘speed to data’, and ‘be more virtual’. These are absolutely real pressures, and it is likely no sector exits a time of financial hardship as it entered it. Evolving to adopt these desired attributes will build on some experiences of the past. Neither virtual biotech companies nor outsourcing to reduce cost or increase speed are new by any stretch of the imagination. Equally, the drive to scale-up UK biotechs, both politically to drive economic development and commercially to increase investor returns in the UK, remains strong yet still faces the same challenges. It should be noted that policy developments at MHRA, the UK government and others are seeking to address several of these barriers.

Is this a systemic consequence of starting UK biotechs early?

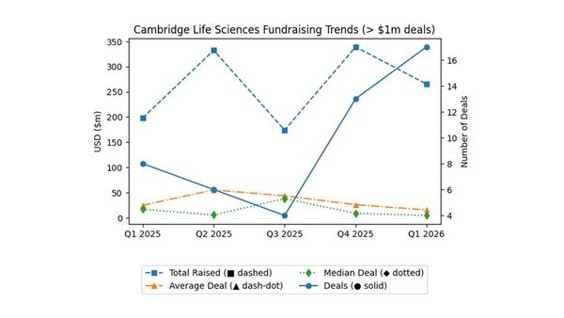

The UK, particularly locations such as the Cambridge-London corridor with a depth of entrepreneurship and experienced investors, remains a location where pre-seed and seed capital can be raised. This was evidenced by multiple £1M+ funding rounds already in Q1 2026 in the Cambridge region, described by Paul Hughes, BDO, recently in Business Weekly, including the following summary figure.

Building a £1M Bridge or Pier?

There is room for concern that when companies and/or technologies are driven towards private capital so early, the funding is not sufficient to bridge the gap to the follow-on venture rounds. With expectations of the data package, investors or licensees/buyers seemingly increasing, the ability to secure key validation data early is critical. Whether one argues it is a lack of proof-of-concept funding, low risk appetite of follow-on investors or simple market dynamics when the supply of ideas outstrips available capital, maybe there is always a feeling of an equity funding gap irrespective of stage.

The nature of early-stage biopharma and drug discovery may mean that the early start is leaving a chasm to bridge to follow-on investment preparedness. This could explain why the current reduction in employment and scaling is most acutely being felt by the preclinical drug discovery sector compared to other less capital and time resource disciplines in Life Sciences. It could be defined more as a stage of technology development and consequently a commercialisation readiness matter as described by Triple Chasm, illustrated below, than a capital availability issue.

Faster, Better, Cheaper

Deal flow at the medium to later stages of innovative medicines is dynamic and positive. Evidenced by multiple >$1Bn M&A transactions, large private capital venture rounds and a steady flow of IPO activity. Securing a share of that available capital is now a global game, and the competition is thus fierce. Speed to high-quality and trusted de-risking data is a large advantage, especially if delivered with the capital efficiency sought after by the investors. Much has been reported, discussed and debated about the impact China’s continuing realisation of their long-term innovation plans is having on the cost and speed competitiveness of established Western bio-innovation hubs. The dynamic plays to the fundamental business value proposition of enabling clients and partners to achieve their goals faster and/or better and/or cheaper.

It would be unthinkable to believe locations such as the Cambridge-London corridor could out-compete China on some of these aspects. It is equally the case that the world-class research and innovation in that UK region continue to fuel invention and creativity in meeting unmet medical needs, and there is an immensely strong ecosystem that supports new venture creation and entrepreneurialism. The question thus remains of how potentially the Cambridge-London ecosystem can compete to create value that attracts investors whilst narrowing the gap over aspects where China and other locations excel. The region should not be unconfident of global competition in areas of strength. For example, the depth of invention, innovation and entrepreneurialism in locations such as Greater Boston and San Francisco has not left the cluster without successes.

Efficiency, speed and planning though are ever increasing masters to obey so this may be the appropriate juncture in time to consider addressing structural ecosystem changes and processes that may help and could include the following:

- Ideation to Invoice Planning: Greater commercialisation readiness (or clear path to it) discipline applied at the ideation stage before venture creation and seed investment. Harnessing the collective knowledge and experience of our community to deliver this from the get-go could be highly beneficial. No plan ever runs smoothly, but generating a route map of dots to join in order to assess the technical and commercial feasibility if all goes well at least provides investors with the comfort of knowing there is a feasible execution plan if all goes well enough.

- Think Global: Mitigating cash burn rates by minimising operational costs and headcount by leveraging the available external resources has merit. As mentioned, there is a global supply chain of options to make the most of, choosing particular ecosystems and providers that are best fit against expertise, capacity, speed and cost criteria.

- Sifting for (Bio)Diamonds: Acknowledging investors, whether financial or corporate, are swamped with opportunities, creating a regional system to triage the created investment opportunities robustly and independently affords a mechanism to select, spotlight and support the very best. Doing the sifting for the investors delivering advantages in catalysing meaningful, lower friction engagement and deal flow.

- Pitching Up: Once selected, enabling those selected companies to be presentation=prepared, due diligence ready and effectively connected to fundraising and dealmaking environments could shorten the finance-raising cycle and preserve technology development momentum.

Has the Question Changed?

With the higher than usual vacancy rates in lab space, a relatively loose and experienced talent pool available and the opportunity to select whether to buy, borrow or build expert capacity in a global context, perhaps now is an ideal time to develop a biotech company in a prime location such as Cambridge or London if the investment is available. How to deploy seed and early-stage capital to create the value proposition to secure the required further investment is perhaps the part of this jigsaw that is the moose needing to be put on the table, taking a collaborative rather than competitive approach to international players.

It may thus be the case that founding entrepreneurs are now asking a different question. This ability to stay lean and capital efficient by leveraging global excellence and capacity for quality, speed and cost benefits means investment can go further, allowing the nascent company to truly build a bridge to follow-on finance rather than a pier into an equity gap. So perhaps the question has changed from ‘Can I build my company here?’ to ‘Can I build my company everywhere from here?’

Supporting Our Members in the New World of Bio Innovation

One Nucleus, proud to be located in such a brilliant bio innovation hub as the Cambridge-London corridor, remains fully focussed on aligning with the better, faster, cheaper aspirations. First, addressing how we deliver our local activities, for example, merging the annual Genesis conference and annual Awards events to reduce cost and diary congestion for our members. Second, by continuing to build those increasingly important international bridges, for example, through the annual Boston Bootcamp, we are confident both our members and One Nucleus will be best placed for future success. Acting locally, thinking globally and being collaborative runs through the DNA of our ecosystem. It also runs through the DNA of One Nucleus.